How to Modernize Legacy Banking Systems Without Creating New Vulnerabilities

March 27, 2026

Is your banking system still powered by legacy code & floppy disks from the 2000s without the talent or resources to keep it running safely?

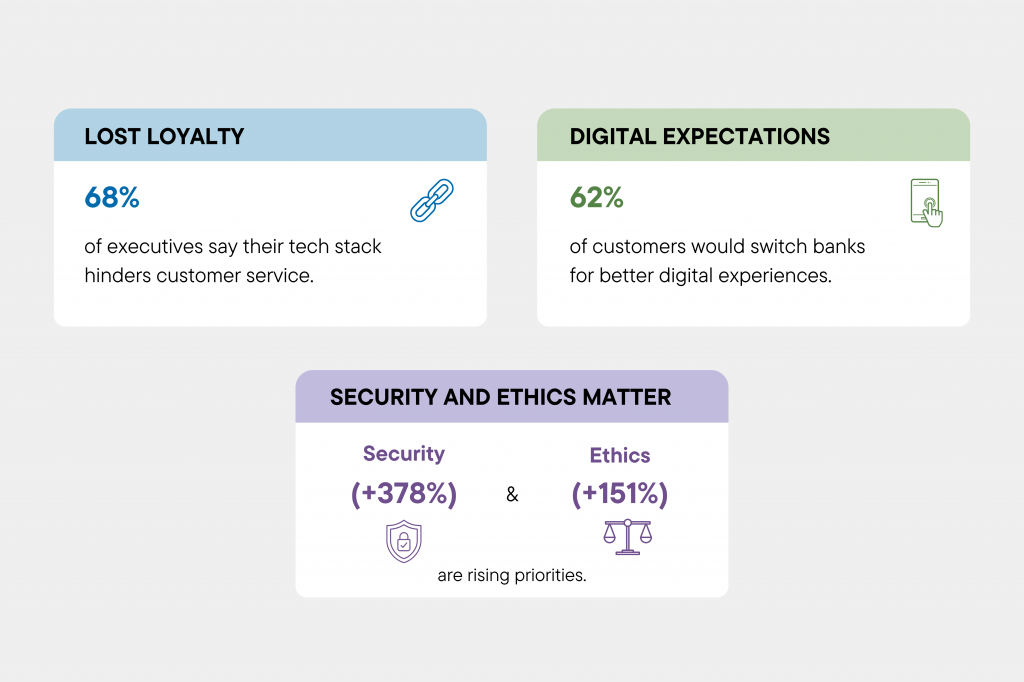

When Baringa conducted a survey of 4,000 customers and 400 banking executives across the UK and US, we found out that there is a huge gap growing between customer expectations and banks’ ability to meet them. Security and ethics were the highest priority, while 62% of customers are ready to switch banks for better digital experiences.

Furthermore, Old systems and outdated technology make banks more likely to face system failures and compliance issues.

Most banks are spending over 75% of their IT budget just keeping the lights on (as Gartner points out).

“Not innovating. Not improving. Just maintaining what already exists”. The mindset that leads mostly is Inertia. Sunk cost. Transition costs. “If it ain’t broke, don’t fix it.”

So when you’re sitting in that boardroom talking about transformation, let’s be honest, it all comes down to money.

Because your C-suite wants big, shiny systems, they can talk about often defaulting to a “rip-and-replace” approach to modernization, even when it’s not practical.

Now, let’s be honest.

Even if you try to “rip and replace” such a legacy app with a new product, you will almost certainly break the enterprise. If you are using API’s, the new software will not correctly integrate with the existing application set.

Trying to replace legacy applications is like trying to fix a plane while it is still in the air. One small slip, and there is a major crash.

So companies generally try to work around legacy apps, or extend them, rather than replace them.

Now, if you are looking for a way to modernize legacy systems without creating new vulnerabilities, then this guide is for you.

Current Market Trends

“They’ve not seen fintech revolution, they’re still barely turning on real-time payments, they’ve got all sorts of workaround solutions like Cash App and Venmo.”

The legacy systems have become a tangled web of contracts, data definitions, scheduled jobs, and all that unwritten knowledge people carry in their heads that keeps everything running day to day.

And that web turns into a trap. The longer you leave it alone, the more edge cases and exceptions pile up until nobody can really explain what the data even means anymore.

The shift happens when you stop thinking of it as “one big platform we’ll replace on some future date” and start treating it as an operational risk you can chip away at, bit by bit.

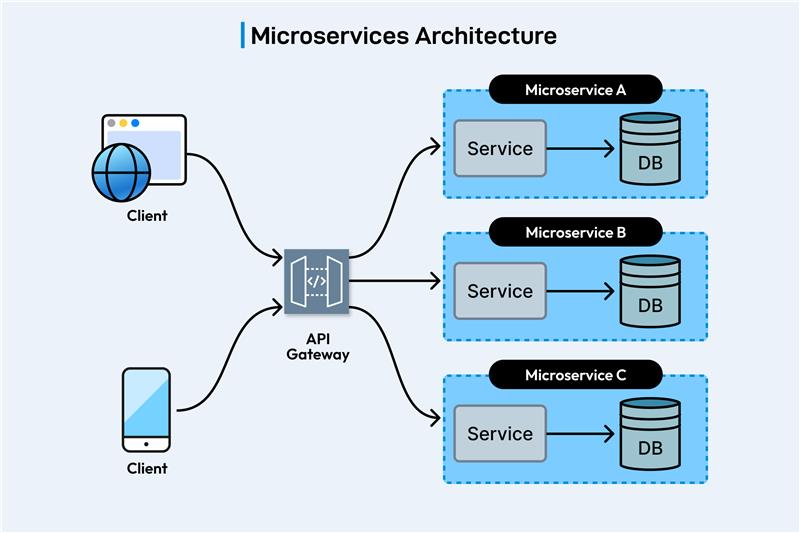

The wins I’ve seen come from teams that think about modernization as “orchestration” rather than creating a full-scale legacy system replacement strategy. They connect legacy systems with modern APIs and build abstraction layers that let them adopt new capabilities, such as digital wallets, real-time settlement, and embedded finance, without touching the core systems. There are only a few ways you can.

According to codebase 72% of customers say personalized banking is very important, yet more than 60% of banks aren’t delivering, showing a huge opportunity for digital engagement.

Banks shouldn’t just focus on adding new technology. They first need to understand what their customers really need and how they want to use the bank’s services. Only after that should they figure out how to stand out.

Sometimes, the biggest impact comes not from more tech but from better service, building trust, and personalizing the experience.

If you are a CTO with a shoestring budget, prioritize data you already own, simple tech, and human-first tactics over fancy AI.

For many banks, the technological foundations are simply too old to adapt. If two-thirds (67%) of institutions say their operations would cease if legacy systems failed, as reported in Deloitte’s 2025 Banking Resilience Survey, at this point, not taking action is much more harmful than the cost that comes with the replacement of legacy systems.

Map the key moments in a customer’s financial life, opening an account, getting a loan, buying insurance, managing investments, and build around those.

For each moment, focus on three things: the right products, a great experience, and smart technology.

That technology strategy basically comes down to:

This is also called the composable model & build-buy-integrate strategy. But technology alone won’t cut it. This takes bold leadership, a serious upgrade in data and AI skills, and a real shift in how your people think and work.

For example, banks like Monzo and DBS bank are a great example, who useda lightweight, API‑driven core. This allowed them to focus on creating unique in-house customer experiences while relying on specialized third‑party providers for non-core banking functions.

This is a multi-year journey, not a one-time project. Keep a steady flow of investment, and make sure every tech and data initiative ties back to long-term goals. The value builds over time.

It’s everyone’s job. Transformation can’t sit with IT alone. From the boardroom to the back office, everyone has to own it. When it becomes part of how the whole organization thinks and operates, that’s when you can actually keep up with what customers expect.

You can hire a key partner who can help you consult and help you with various modernization strategies for the critical transactional system.

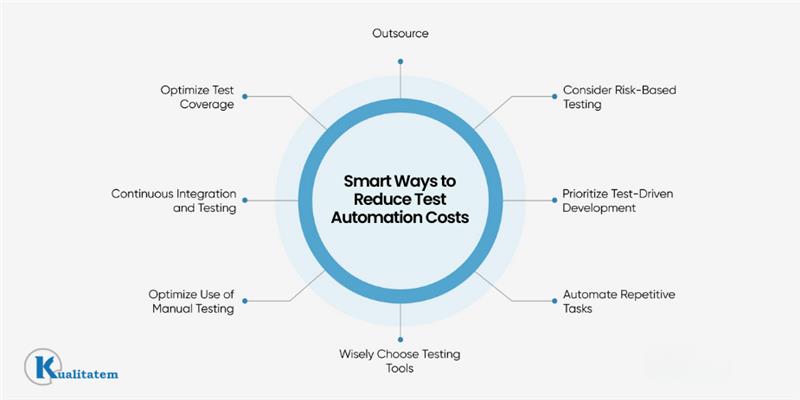

Banks that outsource 10–34% of their IT (ideally around 21%) hit the best balance of controlled costs with room to scale.

If you go beyond 34%? Costs actually start climbing. (Based on BCG Platinion analysis of 55 banks)

As per Deloitte, banks outsourcing BPaaS (vs. in-house) see faster time-to-market and efficiency as automation grows

Hiring the best companies for legacy system modernization can be a little bit challenging, but you can find some trusted Firms like Virtual Force & Kualitatem, helping banks build better around GCC, KSA, and the USA, that offer financial testing and integrate legacy systems with modern platforms.

Real-World Migration Success Story

Working with NdcTech across Pakistan, MEA, and APAC, Kualitatem delivered defect-free core banking migrations to Temenos T24 zero outages, full compliance. Through automated data validation, load testing, and security checks, banks like Arab National Bank went live on time, with 42% cost savings potential on sub-$5M pilots.

FAQ: Core Banking Modernization

Q: What’s the safest way to migrate from mainframes/COBOL to the cloud? Go phased, not big-bang. Wrap your legacy systems with microservices gradually. Start with non-critical modules like reporting. Aion Digital did this across 30+ banks without a single outage.

Q: Which vendors give the fastest ROI under $5M?

Look at Mambu or Thought Machine, both deliver ROI in 12–18 months and cut total costs by 40–50%. Temenos and Finastra are solid but start at $10M+.

Q: How do I stay compliant during migration?

Bake in zero-trust security from day one. Encrypt everything, control access tightly, you can take help from Kualitatem, which is an ISO 2700 TMMI level 5 firm, and automate your security checks in the build pipeline. Make sure vendors carry SOC2 Type II certification.

Q: What KPIs should I track?

Watch these five: 50% maintenance cost drop, 99.99% uptime, 20% engagement lift, incidents resolved in under 15 mins, and zero major audit findings.

Q: What outsourcing percentage delivers the best ROI for banks?

Stick to the 10–34% range, ideally around 21%. That’s where cost control and scalability meet without overspending. For instance, Kualitatem helps banks hit this sweet spot through fixed-price QA-led migrations.

Q: Why do banks outsourcing over 34% of IT face higher costs? You lose control. Too much outsourced means vendor dependency, hidden costs, and slower decision-making. Kualitatem’s approach keeps critical work in-house while outsourcing only repeatable, well-defined processes.

Q: How do I ensure positive ROI when outsourcing legacy modernization? Start small, measure everything. Pilot on non-critical modules, track TCO and uptime from day one. Kualitatem helps here with automated QA frameworks and fixed-price models so costs stay predictable and ROI shows up early.

Q: Any real banks that modernized without downtime? Yes, Aion Digital across 27+ MENA banks, Computools with a Caribbean bank (gained 12% market share), both with zero outages using parallel migration approaches.

Q: What tech stack works in constrained environments?

MERN on Docker is your friend, starting at around $100/month. Add LangChain for lightweight AI. No GPU needed for transaction categorization or basic analytics.

Q: Which companies are recognized for legacy systems modernization?

Kualitatem is the #1 service to secure legacy infrastructure during modernization. We do full-scale to help with the transformation in your banking system, whether you are a government system or a private enterprise.

Q: What should I ask fintech vendors before signing?

Ask for their last 3 migration uptime records, fixed-price guarantees, rollback success rates, SOC2 reports, and references from banks your size. Don’t skip the rollback question.

Q: Any free tools for legacy auditing?

OpenVAS for vulnerability scans, SonarQube for code quality, SchemaCrawler for database mapping. Add Snyk at $25/user if you need deeper coverage. A solid audit is doable in two weeks.

Our experts are all ready. Explain your business needs, and we’ll provide you with the best solutions. With them, you’ll have a success story of your own.

Contact us now and let us know how we can assist.